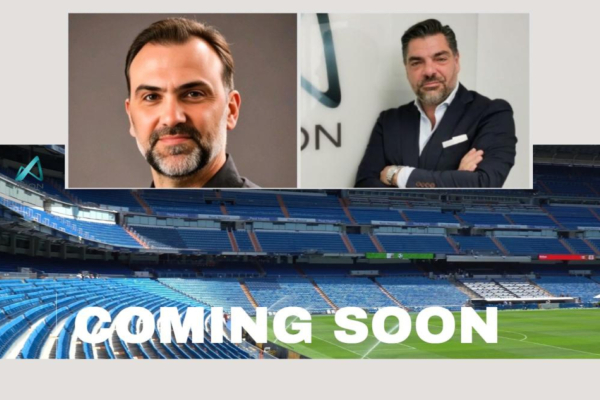

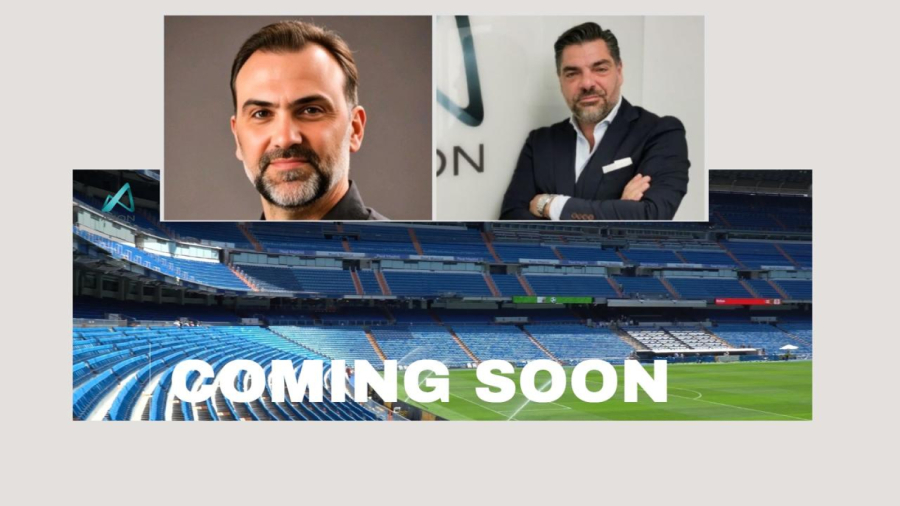

Aeon Acquisition I Corp., a special purpose acquisition company led by Greek entrepreneur Dimitris Mallios and sports agent Giorgos Panou, is encountering mounting complications tied to legacy business dealings, raising questions about its ability to execute an ambitious plan to raise at least $250 million on Nasdaq and invest in Europe’s professional sports and entertainment sectors.

The issues surfaced in a recent annual filing with the U.S. Securities and Exchange Commission, which detailed legal and financial uncertainties surrounding the company. Aeon is structured as a so-called blank-check company, meaning it has no operations, revenue or defined acquisition target. Instead, it aims to raise capital from public markets and later identify a business to acquire—an approach that surged in popularity earlier in the decade but has since drawn increasing skepticism after a wave of underperforming deals.

The company’s leadership blends finance and sports industry experience. Mr. Mallios, its founder and chief executive, is known in Greece for his appearances on television’s “Dragons’ Den.” He is joined by Chief Investment Officer Mr. Panou, a prominent figure in international sports management whose clients have included NBA star Giannis Antetokounmpo. Other senior executives include Chief Operating Officer Victor Klinefelter, a former executive at Philip Morris International, and Chief Financial Officer Alan Lewis.

Despite that lineup, Aeon remains at an early stage and has yet to complete an initial public offering, leaving its fundraising plans on hold. At the center of the delay is a legal dispute involving Mr. Mallios and Chardan Capital Markets, a U.S.-based investment bank that previously provided capital-raising services to entities linked to Aeon’s broader corporate network.

Chardan has claimed more than $15 million in fees under agreements dating back to 2023 and 2024, arguing it is entitled to compensation for services already performed. The dispute escalated in February, when the firm filed for arbitration against Aeon, Mr. Mallios and affiliated companies, a move that threatened to complicate or derail the planned listing. Aeon sought to block the arbitration in New York state court, while Mr. Mallios and a related entity agreed to indemnify the company against potential liabilities. The parties reached a tentative settlement in late March that could clear the path for the IPO—but only if the offering is completed by May 25.

Under the agreement, Chardan would take on the role of lead underwriter, with D. Boral Capital acting as co-lead. The two firms would split fees and other financial benefits evenly, including underwriting commissions and potential future deal-related income. The deal also grants both sides shared rights to participate in future transactions involving Aeon.

The settlement carries a strict condition: if the IPO is not completed by the deadline, the agreement automatically lapses and arbitration resumes, reviving Chardan’s claims. If the listing proceeds, however, all legal actions are to be withdrawn within days, and prior agreements between the parties would be terminated.

Aeon has told regulators that proceeds from the IPO would be placed in a trust account and not used to cover past obligations, a standard safeguard in SPAC structures but one that may not fully ease investor concerns given the ongoing dispute.

The situation leaves the company in a bind. Without completing the IPO, it cannot resolve the legal overhang; yet the existence of that overhang may deter investors needed to make the offering a success. For a firm seeking to raise hundreds of millions of dollars to pursue acquisitions, the lack of financial clarity presents a significant hurdle.

Whether Aeon can overcome those challenges and secure a Nasdaq listing in the coming weeks remains uncertain. Its prospects may hinge on whether Mr. Mallios and Mr. Panou can persuade investors that the company’s past liabilities will not weigh on its future ambitions.